STEP 03

Register for an MyGovId if you don’t have one

STEP 06

Lodge your trust tax return!

STEP 04

Connect LodgeiT to the Australian Tax Office

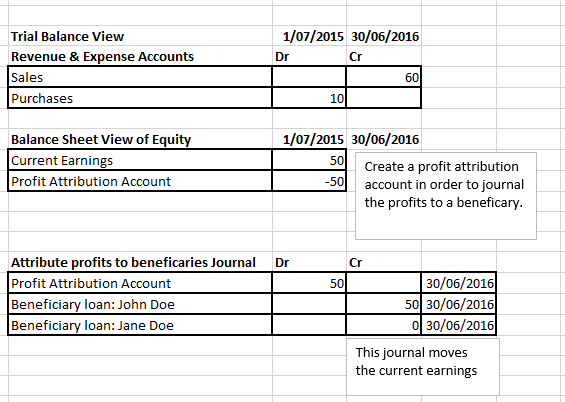

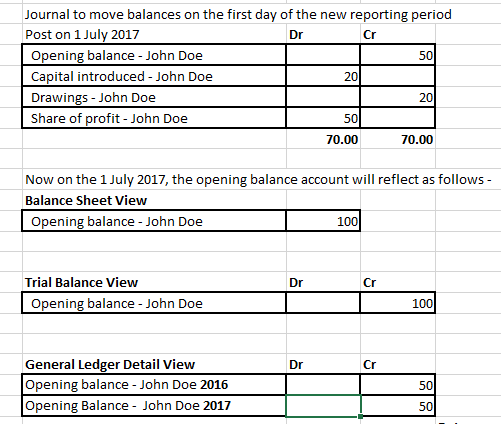

Bear in mind that most accounting software is not designed to roll the beneficiary loan account sub-ledgers and therefore you will be required to post an additional set of manual journal transactions to close out the balance sheet at the end of any given reporting period.

Now for our trust, we need to allocate profits to the respective beneficiaries in accordance with the trust distribution minutes using the following journal at the end of any given reporting period i.e. financial year.

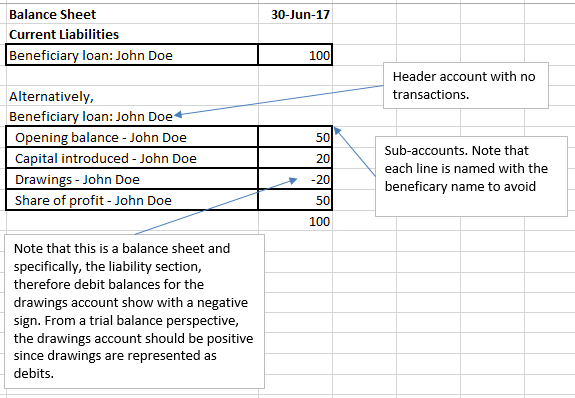

LodgeiT provides special purpose accounts that allow you to easily reflect the primary trust beneficiary accounts including profit, drawings / maintenance payments and capital / funds introduced.

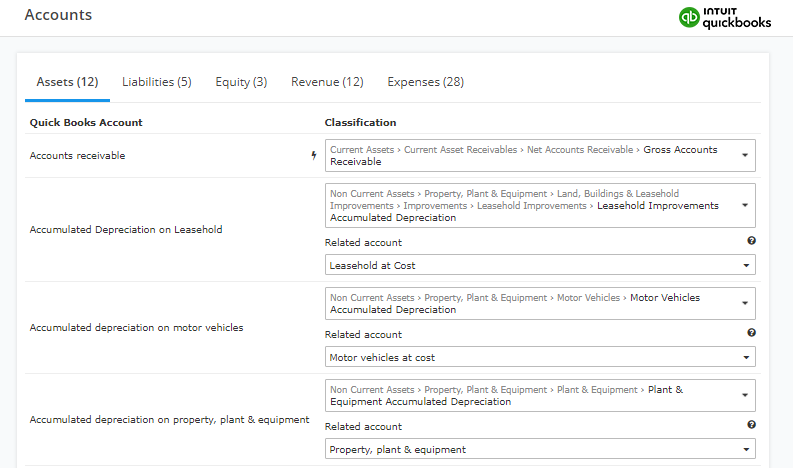

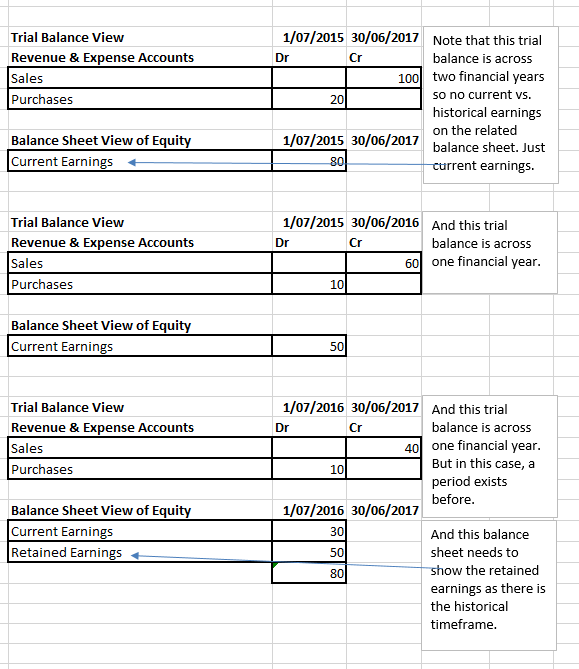

Cloud-based accounting systems including Xero, MYOB Account Right Live & QuickBooks Online are designed for profits to accumulate and reflect in the equity section. The following views of trial balance & equity sections shows only the relevant parts.